Donald Trump’s 2025 Tariff Strategy

A Contrarian Take on Trade History and Rebalancing

If you do not change direction, you may end up where you are heading

— Lao Tzu

It’s April 2025 and President Donald Trump’s new tariff offensive – a blanket 10% import tax on all countries, with steeper rates on nations running big trade surpluses, has upended the post-WWII trading order. Global markets recoiled at this “full rejection of the post-WWII system of mutually agreed tariff rates”(reuters), with the S&P 500 plunging and pundits invoking the specter of Smoot-Hawley. Indeed, the average U.S. tariff is now estimated at 29% – the highest since 1900 (theguardian). Critics predict higher prices, job losses, and even recession as a result (theguardian). Yet a contrarian analysis, grounded in global economic history from Bretton Woods (1944) to today, suggests Trump’s hardball trade strategy may be a long-overdue strategic recalibration. To see why, we must trace how the U.S.-led trade system born in the Cold War no longer serves American interests, and how decades of missed opportunities and entrenched corporate interests kept that system on autopilot.

In what follows, we’ll revisit the timeline of key trade milestones since 1944, examine how U.S. policy designed to win the Cold War led to persistent imbalances, and explore why successive administrations failed to update the rules after the Soviet Union fell. We’ll also look into how corporate lobbying has resisted meaningful reform while countries like China, Germany, and South Korea leveraged the status quo to their advantage. Finally, we’ll break down why most analysts may be missing the method in Trump’s tariff “madness” – overlooking the strategic nuance due to economic orthodoxy and political polarization, and what a contrarian sees in the 2025 tariff strategy that could ultimately make it successful despite the initial panic.

From Bretton Woods to 2025: Key Trade Milestones

To understand the context, it’s useful to chart a brief timeline from the mid-20th century trade order to the present tariff clash:

1944 – Bretton Woods Conference: The Allied powers meet in Bretton Woods, NH to design a postwar economic system. The U.S., emerging as the global economic leader, champions freer trade and stable currencies to avoid the protectionism of the 1930s. The conference creates the IMF and World Bank, laying the foundation for an open, U.S.-led international economy (history.state.gov).

1947 – GATT Established: 23 nations sign the General Agreement on Tariffs and Trade, cutting tariffs and codifying trade rules. GATT becomes the de facto framework governing world trade for nearly 50 years, as the U.S. opens its huge domestic market to help allies rebuild. Early Cold War leaders believed American allies’ “economic recovery” and “export markets – particularly the huge U.S. market” – were vital for stability and loyalty (usa.usembassy.de).

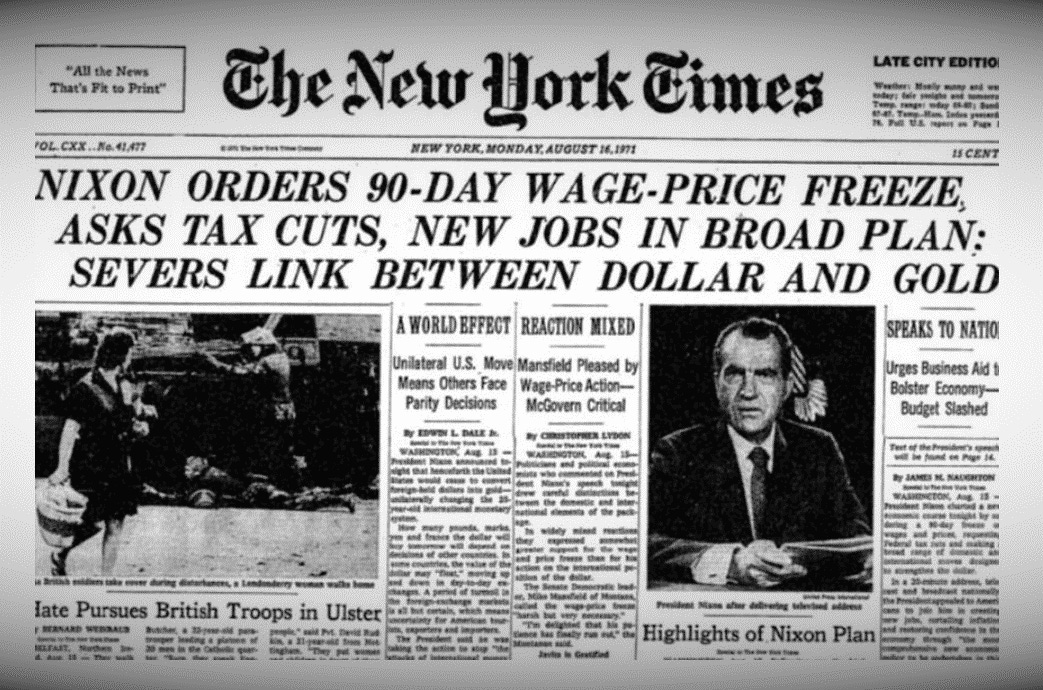

1971 – End of Bretton Woods: President Nixon suspends dollar-gold convertibility, ending the fixed exchange rate system. Currencies begin to float, introducing volatility and new challenges (like currency misalignments) to global trade (history.state.gov). The postwar “golden age” of U.S. industrial dominance wanes, as Western Europe and Japan catch up and American trade surpluses shrink.

“Gold is out, vibes are in.” 1980s – Rising Trade Tensions: Huge U.S. trade deficits emerge with Japan and West Germany. The Reagan administration deploys targeted measures, e.g. the 1985 Plaza Accord (forcing a stronger yen) and tariffs/quotas on Japanese electronics, cars, and even motorcycles, to defend U.S. industries. These managed-trade interventions preview Trump’s approach, albeit on a smaller scale.

1989–1991 – Cold War Ends: The fall of the Berlin Wall and the dissolution of the Soviet Union remove the original geopolitical rationale for U.S. trade generosity. However, instead of overhauling the system, the U.S. doubles down on the existing free-trade paradigm in the 1990s.

1994/1995 – NAFTA and the WTO: The U.S., Canada, and Mexico enact the NAFTA free trade agreement in 1994, accelerating North American integration. In 1995 the World Trade Organization (WTO) replaces GATT, expanding global trade rules to more countries and issues (services, intellectual property, etc.). The U.S. leads these efforts, expecting that more open markets will spread prosperity and democracy.

2001 – China Joins the WTO: The U.S. grants permanent normal trade relations to China, paving the way for Beijing’s WTO entry. Hopes are high that China will liberalize. Instead, China practices mercantilism – combining high productivity with low wages behind protective policies – and the WTO admission “worked for Chinese development and for American capitalists” while devastating many U.S. factories (prospect). This marks the start of a massive U.S.–China trade imbalance.

2000s – Deepening Imbalances: Year after year, the U.S. runs large trade deficits (peaking at over $760 billion in 2006), especially with China, Germany (via the EU), Japan, Mexico, and South Korea. Export-led economies relish access to America’s consumer market, often while restricting imports to their own. U.S. policymakers mostly tolerate this, reflecting the entrenched pro-trade consensus and corporate benefits from globalization.

2016 – Populist Backlash: In a shock to the establishment, Donald Trump wins the presidency on an “America First” platform, channeling anger in industrial states over job losses. Trade is a central issue: Trump calls NAFTA “a disaster” and accuses China of “raping” the U.S. economy. This political earthquake underscores that the post-Cold War trade regime left many American workers behind.

2017–2019 – Trump’s First-Term Salvos: The Trump administration imposes tariffs on steel and aluminum (including on allies), citing national security, and levies tariffs on about $360 billion of Chinese imports over intellectual property and trade abuses. Allies howl and China retaliates, but Trump holds firm. He also renegotiates NAFTA into the USMCA (implemented 2020), which modestly updates rules on autos, labor, and digital trade. By 2020, U.S. tariffs average ~19% on Chinese goods (vs. 3% pre-Trump) and a few percent on other imports – the biggest protectionist shift in decades, though still limited in scope.

2021–2024 – Stasis and Shifting Rhetoric: The Biden administration leaves most of Trump’s tariffs in place (notably on China) and articulates a “worker-centered trade policy,” but pursues no major tariff reductions or new free trade deals (wita.org). Instead, Biden focuses on industrial policy (e.g. the CHIPS Act and clean energy subsidies) and “friendshoring” supply chains away from China. U.S. trade strategy drifts without fundamental reform to the global system, as political appetite for status-quo free trade wanes across the spectrum.

2025 – Tariff Shock under Trump 2.0: Returning to office, Trump unleashes a sweeping tariff strategy. An across-the-board 10% import tariff takes effect April 2025 on virtually all countries (with narrow exceptions for essentials like crude oil, pharmaceuticals, and semiconductors) (reuters). On top of that, “reciprocal” tariffs ranging from 11% up to 50% are slated to hit 57 countries with large trade surpluses or protectionist policies. For example, EU goods face a 20% duty, Japanese goods 24%, South Korean 25%, Chinese goods 34% (bringing total U.S. tariffs on China to ~54% when combined with earlier duties. Even close allies like the UK, Canada, and Israel are not spared some level of tariff. This dramatic move, dubbed “Liberation Day” by Trump, represents the most radical U.S. trade shift in a century, igniting panic among investors and drawing global retaliation threats.

With the stage set, we can now analyze why the post-1945 trade architecture, which worked for a Cold War era, became increasingly misaligned with U.S. interests, and how Trump’s tariffs aim to correct course (Spoiler: the verdict’s still out, but the strategy behind them deserves a closer look).

Cold War Trade Strategy: Building a Free World (and Its Costs)

From the outset of the postwar order, American leaders consciously designed trade policy as a tool of geopolitics. In the late 1940s and through the Cold War, the U.S. used access to its vast domestic market as both carrot and stick to solidify alliances against the Soviet bloc. As a State Department history notes, many U.S. officials believed “the domestic stability and continuing loyalty of U.S. allies would depend on their economic recovery,” which meant those nations “needed export markets – particularly the huge U.S. market – in order to regain economic independence and achieve growth.” The U.S. thus “supported trade liberalization” and was “instrumental in the creation of the GATT” to promote this goal (usa.usembassy.de). In essence, America accepted that it would be the importer of last resort, fueling allied growth, in exchange for political allegiance in the fight against communism.

This grand strategy meant the U.S. often tolerated—even quietly encouraged—its allies’ protectionist and mercantilist practices as the cost of Cold War loyalty. Through the 1950s and 60s, East Asian partners like Japan and South Korea ran state-led industrial policies and maintained closed markets, but Washington let it slide. America still had a massive economic lead, and if a few tariffs or subsidies helped allies grow strong and stay on-side, so be it. Japan, for example, became an export powerhouse behind tariff walls and informal barriers, yet enjoyed unfettered access to U.S. consumers. Western Europe played a similar game. West Germany rebuilt its industry under the Marshall Plan, ran an undervalued currency, and shipped cars, machinery, and chemicals straight into the American market, all under the protective umbrella of Pax Americana.

By the 1970s, however, the landscape was shifting. The U.S.’s huge economic advantage was eroding as allies became industrial giants themselves. The Bretton Woods currency system collapsed in 1971, U.S. manufacturing supremacy waned, and trade deficits began to appear. Still, Cold War logic predominated: American strategists largely viewed trade concessions as a reasonable price for alliance unity. Even as the U.S. ran trade gaps with Germany and Japan, it pressured them only episodically (e.g. the 1980s yen revaluation) but never fundamentally reset the system of mostly one-way openness. The result was a kind of “one-sided free trade” regime: allies enjoyed relatively free access to U.S. markets, while often maintaining higher barriers or mercantilist policies at home, all under the U.S. security umbrella. This structure achieved its primary aim, a prosperous “Free World” girded against Soviet influence, but its economic costs to the U.S. became apparent later, in lost industries and mounting debt, once the geopolitical rationale disappeared.

After the Soviet Fall: Missed Chance to Redefine Trade

The end of the Cold War in 1989–91 was a turning point that, in retrospect, the U.S. failed to seize for trade reform. With the Soviet threat gone, many expected a “peace dividend” and perhaps a tougher line on allies’ trade surpluses or on China’s rising mercantilism. Instead, the 1990s saw an expansion, even an acceleration, of the old paradigm rather than a rethinking. Washington, intoxicated by triumphalism and neoliberal economics, treated free trade as an article of faith. President Clinton’s tenure epitomized this: his administration backed NAFTA’s implementation and led the creation of the WTO, integrating more countries into the U.S.-designed system on the assumption that more trade was inherently good. In 2000, Clinton pushed for China’s entry into the WTO, despite China’s state-led model. This decision proved fateful. China, still a tightly controlled and state-led economy, was granted full WTO membership on the hope that integration would spark liberalization. Instead, Beijing played the system. Mercantilist policies, industrial subsidies, and currency manipulation went largely unchecked, and China used its WTO access to become the world’s manufacturing base. American corporations profited, Wall Street applauded, and U.S. industrial towns were hollowed out. In effect, Washington extended a Cold War-era gift, open access to the American market, to a post-Cold War competitor. And China took full advantage.

American policy after the Cold War failed to update the rules of the game, even as global conditions shifted. No meaningful constraints were imposed on currency manipulation, industrial subsidies, or chronic trade surpluses. Countries like Japan and Germany continued to run large surpluses with the U.S., and Washington’s response was mostly silence. Germany, protected by the euro, which kept its exports cheaper than a Deutsche Mark would have, kept selling far more than it bought. By the 2010s, its strategy of holding down wages and domestic consumption to boost exports was clearly imbalanced. A handful of surplus economies continued to ride the rhetoric of free trade while running what were effectively mercantilist playbooks. And once those surpluses accumulate, there is little incentive to adjust.

Meanwhile, U.S. leaders, preoccupied with European diplomacy and the War on Terror, rarely applied pressure. Successive presidents stuck to the status quo. George H.W. Bush and Clinton championed free trade. George W. Bush imposed a few tariffs, like the 2002 steel duties, but quickly backed down under WTO pressure. Obama expressed concern over job losses, but poured his energy into the Trans-Pacific Partnership—a sweeping trade deal that mostly extended the existing framework, with some updates around labor and environmental standards. None of them fundamentally reworked the core trade bargain: American market access in exchange for... not much.

Why did U.S. administrations shrink from major trade reform even as the Cold War rationale evaporated? Partly due to ideological consensus: by the 1990s, “free trade” had become gospel in both major parties, and admitting the system had flaws was seen as heresy. There was also a hopeful (or naive) view that globalization would eventually convert even authoritarian capitalist countries into fair players. But a more concrete reason was the influence of corporate interests and Wall Street – which had become deeply invested in the status quo of hyper-globalization.

The Corporate Lobby and the Globalization Inertia

While American factories closed and industrial towns hollowed out in the 1990s and 2000s, powerful corporate and financial interests were cashing in. These groups formed a well-organized lobby that worked to lock U.S. trade policy into place, resisting any meaningful course correction. For multinationals and banks, the system worked just fine. It let them offshore production, arbitrage labor and environmental standards, and boost margins, even if the U.S. manufacturing base was slowly being gutted.

Trade agreements during this era increasingly reflected corporate wish lists. Using tools like the 1974 Trade Act’s fast-track authority and a network of trade advisory committees, lobbyists shaped deals to serve corporate priorities. Entire chapters were devoted to intellectual property protections, investor-state dispute mechanisms, and financial services access. Provisions that couldn’t pass through Congress were quietly embedded in trade deals, turning them into corporate policy by other means. This wasn’t free trade, it was trade tilted toward capital.

Financial firms helped craft WTO rules that pried open foreign markets for Wall Street and Big Tech. The concept of “trade in services” was introduced, pressuring countries to liberalize their banking and insurance sectors. The result was a global trade regime that safeguarded capital, intellectual property, investor rights, & financial access, far more than it protected labor.

It’s no coincidence that the U.S. now runs a $1.2 trillion annual deficit in manufactured goods but a $278 billion surplus in services, mostly driven by finance and technology. One side of the deal enriched boardrooms. The other emptied out the heartland.

Given this alignment of incentives, corporate America vigorously resisted any move toward protection or managed trade. The big industry associations, the U.S. Chamber of Commerce, Business Roundtable, National Association of Manufacturers – became staunch guardians of the free-trade status quo. When Trump emerged in 2016 threatening tariffs, these groups panicked. In 2018, the Chamber of Commerce famously launched a campaign against Trump’s tariffs, arguing tariffs “won’t solve these problems, and will only raise prices for American families” (uschamber). By 2025, when Trump announced the new tariff package, the Chamber was reportedly even considering suing the administration to block it (finance.yahoo). Publicly, business lobbyists issued strongly worded statements against Trump’s trade action (politico)(nam). Privately, however, they were in a bind. Corporate leaders still prioritized tax cuts and deregulation, wins they had secured under Republican leadership, and didn’t want to jeopardize their influence within the party. Open confrontation wasn’t in their playbook. So instead of trying to stop the tariffs outright, they looked for workarounds. During Trump’s first-term trade actions, more than 4,000 companies flooded the U.S. Trade Representative’s office with exemption requests (npr), hoping to carve out protections for their supply chains. The result was a fragmented, reactive approach (some got relief, most didn’t) that revealed just how disjointed corporate America had become on trade policy. There was no unified front, only damage control.

In sum, corporate and financial lobbying helped lock in the old trade framework, even as its disadvantages to the broader national interest grew. Every time a reckoning loomed, be it the late-80s Japan scare, the post-2008 reassessment, or the populist rumblings of the 2010s, the inertia won out. By the mid-2010s, the U.S. had a trade regime on autopilot: still running on Cold War-era logic (open U.S. market, free-trade pieties) but increasingly out of sync with 21st-century realities. The stage was set for a disruptor to smash the autopilot – and that came in the form of Trump and tariffs.

Structural Trade Imbalances: Who’s Really Dependent on Whom?

A core argument of the contrarian view is that the U.S. has leverage in reshaping trade because of structural asymmetries in the global economy. In plain terms: many of America’s trading partners depend far more on access to the U.S. market than the U.S. does on access to theirs. A quick look at trade as a percentage of GDP for various countries is illuminating:

United States: Exports of goods and services are only about 11% of U.S. GDP (as of 2023) (jpmorgan) – the lowest share among major economies. America’s colossal $25 trillion economy is fundamentally driven by domestic consumption, not exports. (Total trade – exports plus imports, is around 25% of GDP (macrotrends) (ceicdata), relatively modest for a large economy.)

China: Exports are ~14% of China’s GDP (jpmorgan) – down from earlier peaks, but still significant. Crucially, the U.S. is China’s top export customer, buying nearly 13% of China’s total exports in 2023. This makes China vulnerable: a large chunk of its industrial output is ultimately geared toward U.S. consumers.

Germany: Exports equal about 37–44% of GDP (Germany’s national figure was 43% in 2023 (tradingeconomics)). Germany is extraordinarily export-dependent – the most in the G7 – running chronic trade surpluses. It has effectively pursued a neo-mercantilist path: restraining wages and consumption at home to boost competitive exports abroad. As one analysis put it, Germany and a few others “increase exports while hiding behind free trade rhetoric,” and their large surpluses are not accidents but the result of policy choices (americanaffairsjournal). Germany’s economy thus relies on external demand – with the U.S. as a key destination (the U.S. is Germany’s single largest export market as of 2024) (commonplace).

South Korea: Exports are about 38% of GDP (jpmorgan) (and total trade nearly 88% of GDP! (statista)), making South Korea one of the most trade-dependent countries. Like Germany, South Korea’s post-war development was built on export-led growth (often protected by domestic barriers). It sells cars, electronics, ships, etc., globally, again with the U.S. as a major buyer. Seoul, much like Tokyo and Berlin, has long counted on the U.S. market to fuel its industries while enjoying U.S. security protection.

Mexico: Exports about 33% of GDP (jpmorgan), with 75% of those exports going to the United States under NAFTA/USMCA. Mexico’s manufacturing (autos, appliances, etc.) is deeply integrated with U.S. supply chains, effectively an extension of the U.S. industrial base in some sectors. This high dependence gives the U.S. significant leverage (as seen in 2019 when Trump’s tariff threats quickly got Mexico to tighten migration enforcement).

Japan, UK, Canada, etc.: Japan’s exports are ~18% of GDP, Britain’s ~23%, Canada’s ~26%, all higher than the U.S. share. These allied economies are also relatively more reliant on trade with the U.S. (Canada, for example, sends about ~75% of its exports to the U.S.).

The pattern is clear: the U.S. is the least trade-dependent major economy, while many partners are far more export-reliant, especially on the American market. This is the inverse of the common perception that “America needs the world.” In fact, the world economy – in its current form – needs American consumers. Even China, which has a huge domestic market, still relies on selling hundreds of billions of goods annually to the U.S. (and has not yet fully rebalanced to internal consumption). Germany’s mercantilist model, as commentators Pettis and Klein argue, effectively means “German consumers spend less than they earn” and the country doesn’t absorb its own output, so “Germany supplies the demand, a lot of it going to the U.S.” (prosperousamerica). One pithy line from those economists: “The U.S., of course, is the world’s favorite dumping ground.” Cheap foreign goods flood in; the U.S. soaks up the exports that others can’t consume themselves.

Why does this matter? Because it underpins the strategic logic of Trump’s tariff gambit. If the U.S. imposes barriers, countries with high trade/GDP and big U.S.-focused exports stand to lose the most. Their economies and companies will feel pain quicker, potentially forcing them to the negotiating table. By contrast, the U.S. economy, while not immune to trade disruptions, can sustain a hit to imports more readily, especially if it spurs some replacement by domestic production or sourcing from alternative friendly nations. In blunt terms, when an export-dependent country and an import-dependent country get into a trade war, the export-dependent one has more to lose in the short run.

Take China as an example: Trump’s tariffs (in 2018 and now in 2025) hit China where it hurts, its export industries and employment. Beijing can retaliate (and has, with its own tariffs and export curbs (reuters), but China cannot match the U.S. dollar-for-dollar because it imports far less from the U.S. than it exports. Similarly, Germany and South Korea, who count on trade surpluses, have limited leverage aside from diplomatic pressure. This asymmetry was largely ignored by previous administrations who feared rocking the boat. Contrarians argue Trump recognized this underused leverage, the ability of the U.S. to withstand a trade conflict better than most rivals, and he’s willing to use it to force change.

What the Critics Are Missing: Breaking Down the Polarized Debate

The conventional reaction to Trump’s tariffs has been overwhelmingly negative in policy circles and media commentary. It’s worth summarizing the critics’ main points, and then examining what they overlook:

Critic Claim #1: “Tariffs are a tax on consumers and will hurt the U.S. economy.” This is the most common refrain. Indeed, import taxes do raise costs for importers and likely for consumers down the line. Analysts predict the across-the-board 10% tariff will boost inflation and cut growth in the U.S. (the Fed itself warned of this) (abcnews). The Guardian bluntly states Trump’s tariffs “will raise prices, eliminate jobs and shrink retirements”, with American workers paying the dearest price. Many economists cite the 1930s Smoot-Hawley tariff as a cautionary tale, worrying Trump’s move could trigger a global downturn.

Critic Claim #2: “Trade wars harm everyone – there are no winners.” The orthodox economic view is that tariffs and retaliation create a lose-lose situation. The WTO system and multilateral trade deals were built to prevent tit-for-tat protectionism. By smashing these norms, Trump invites retaliation (which has indeed occurred, from China, EU, etc.), and the result could be collapsing exports for all, spooked markets, and strained supply chains. In this view, even if other countries “depend” on U.S. trade, hurting them will also hurt U.S. companies (who export or rely on imported inputs) and consumers (via higher prices). Global supply chains are so interwoven that any attempt to unwind them rapidly is seen as highly disruptive.

Critic Claim #3: “Trump’s strategy is incoherent, rooted in politics not economics.” Many analysts accuse Trump of using tariffs as a blunt political tool, red meat for his base, without a real endgame. They argue his past behavior (raising tariffs, then suddenly exempting certain allies or delaying measures) was erratic, undermining U.S. credibility (theguardian). Some point out inconsistencies: for example, if tariffs are about security, why hit allies like the UK or Israel? If it’s about fairness, why tax countries like Brazil or Australia that run trade deficits with the U.S.? (The administration’s reply is that those deficits would be larger if not for unfair policies.) Critics see a lack of a clear metric for success and fear permanent trade friction that yields no real improvement. They also note Trump’s personal style, dealmaking chaos, could backfire in a complex global trade setting.

Critic Claim #4: “Undermining alliances and global rules is strategically foolish.” Beyond economics, foreign policy commentators worry that Trump’s tariffs alienate allies and cede moral high ground to adversaries. The U.S. spent 70+ years building a multilateral trading system; throwing it into disarray could weaken U.S. leadership. For example, European and Asian allies angered by tariffs might drift closer to China or form their own trade pacts excluding the U.S. China, in turn, has cast Trump’s actions as irresponsible, Beijing quipped “the market has spoken” in criticizing Trump after stock drops. By this view, Trump is strategically myopic, risking the international order for short-term nationalist gratification.

Critic Claim #5: “Any valid grievances (China’s abuses, etc.) are better solved with allies and within rules.” Even those who acknowledge problems with China or Germany’s surpluses argue that unilateral tariffs are the wrong solution. They prefer negotiated solutions: e.g. forming a united front with Europe and Japan to pressure China at the WTO, or using diplomacy to address currency issues. They point out that the U.S. actually won a WTO case against China’s tech theft, or that coordinated action has worked (like the 1985 Plaza Accord on currencies). By acting unilaterally and antagonizing everyone at once, Trump, they say, undermines the potential for collective pressure on the worst offenders.

Given these critiques, why do contrarians still see Trump’s approach as having strategic merit? The answer lies in recognizing certain realities that critics underplay:

First, the status quo was never as rosy as painted. Free traders celebrate the post-WTO era’s low consumer prices and corporate profits, but ignore the immense regional and class disparities it created in the U.S. Whole industries (steel, textiles, electronics, furniture, etc.) were gutted; communities were devastated. Mainstream voices often dismiss this as the inevitable price of progress or blame automation, yet that rings hollow in the communities affected. The political backlash (Trump’s election) was a clear signal that large swaths of America were not benefiting. Critics calling Trump’s tariffs “economic misrule” (theguardian) forget that decades of trade policy misrule led to Trump. Contrarians argue a shock was needed to break the complacency.

Second, gradual or multilateral fixes have repeatedly failed to stem abusive trade practices. Diplomacy and WTO litigation have not stopped China’s IP theft, subsidies, or forced tech transfers in any meaningful way, these issues have been on U.S. agendas since the 1990s with little progress. Germany’s surplus was debated for years in G7 meetings, yet Germany did not materially boost domestic demand. In short, polite requests and minor tweaks didn’t work; something stronger was necessary. Trump’s tariffs are a blunt instrument, but they get everyone’s attention. As one trade lawyer noted, “This is the single biggest trade action of our lifetime…a pretty seismic shift in the way we trade with every country on earth.” (reuters) Sometimes shaking the status quo is the only way to force a real negotiation. Even former USTR Robert Lighthizer (the architect of Trump’s trade policy) argued that tariffs and trade restrictions are the only leverage to make entrenched violators change (wita).

Third, short-term pain can lead to long-term gain – a nuance often lost in hyperbolic media coverage. Yes, tariffs can cause price increases and volatility. But contrarians point out this is the cost of adjustment, and it need not last indefinitely. If tariffs prod companies to shift supply chains or produce more in the U.S., resilience improves. Lighthizer himself acknowledged some short-term economic knock, “a short-term knock if [we want] a long-term knockout blow” to unfair trade (politico). In 2018, despite dire predictions, the U.S. economy did not collapse under Trump’s initial tariffs; unemployment actually hit 50-year lows by 2019 (before the pandemic). This doesn’t prove tariffs are harmless – but it shows the worst-case scenarios are often exaggerated. The markets’ “panic” in 2025 (a record $5 trillion stock wipeout in two days) may similarly prove oversold once businesses adapt and trade partners negotiate exemptions.

Lastly, and crucially, Trump’s tariff strategy is a strategy – just not one his critics acknowledge. Detractors caricature it as ignorant protectionism, but there is an underlying logic: to reorder the terms of trade to favor the United States, using maximum leverage. Trump has explicitly framed this as an “economic revolution” that will be “historic” (reuters). The plan isn’t to tariff forever; it’s to use the shock as bargaining leverage. We see this already in the flurry of responses: U.S. allies and rivals scrambling to negotiate. The White House wants countries to call and make deals. As Kelly Ann Shaw (former Trump trade adviser) noted, many countries will seek to “negotiate lower rates” in response. Trump’s team even announced it as “reciprocal tariffs”, signaling that if countries lower their barriers or fix imbalances, tariffs could drop. In essence, Trump opened negotiations with a big stick, after years of U.S. carrots being ignored.

Consider some early outcomes: Vietnam, which had benefited from factories relocating out of China, suddenly faced a brutal 46% tariff on its goods. Hanoi quickly agreed to urgent talks on a trade deal to avoid those tariffs (reuters). The UK, a close ally now facing a 10% baseline tariff, immediately started discussing an exemption deal (PM Keir Starmer vowed to “help shelter British business” and prioritize a trade agreement with the U.S. (reuters). Japan’s prime minister sought a call with Trump as Japan was hit with 24% duties (reuters). Even Israel, levied at 17%, dispatched officials to Washington to negotiate (reuters). In other words, Trump’s shock therapy is forcing engagement on U.S. terms. Critics who claim he’s isolating America miss that many countries aren’t retaliating in kind but rather coming to the table, because they need access to the U.S. market.

Another overlooked point is that Trump’s tariffs target not just adversaries but friends to eliminate free-riders. This is controversial, but think of it this way: During the Cold War, the U.S. tolerated allies’ trade advantages as part of security agreements. Today, Trump is essentially saying: America’s defense umbrella and wealth can no longer be taken for granted without fair economic exchange. Allies might not like it, but it’s a push for them to consume more and rely less on exporting to the U.S. (In fact, Trump has explicitly linked trade and security in the past, complaining that allies running big surpluses also underpay for defense). The contrarian view sees coherence here: pressure allies economically to either import more from the U.S. or lose some U.S. market access, either outcome reduces U.S. deficits or strengthens U.S. industry. It’s a hardball renegotiation of the postwar deal.

Rebalancing Trade: A New Paradigm in the Making?

Trump’s 2025 tariff strategy, bold as it is, can be interpreted as the first act in forging a new trade paradigm for the post-post-Cold War era. Rather than tinkering around the edges, it attempts a reset: realigning global trade flows, updating terms with allies, and confronting mercantilist powers with the choice to reform or lose the U.S. market. This is essentially a mirror image of the Bretton Woods vision, but inverted for today’s reality. In 1944, the U.S. led in creating rules that opened its market to help others. In 2025, the U.S. is leveraging its market to force others to open theirs (or at least to balance the exchange).

Will it work? The contrarian believes it can, if pursued with a clear goal in mind: to negotiate a series of deals that leave the U.S. with reciprocal trade arrangements, far fewer deficits, and more domestic industry. The tariffs are the bargaining chip. Imagine, for instance, a revised trade deal with the EU where Europe agrees to lower auto tariffs and buy more American LNG or aircraft, in exchange for the U.S. lowering the 20% tariff back down. Or a deal with China where, perhaps, China agrees to strict limits on subsidies and a schedule to reduce its surplus, in exchange for phased tariff reduction. Skeptics say China would never agree, but China has also never faced 54% tariffs on all its exports to its #1 market before. The pain on Chinese firms is immense, and Beijing’s own retaliatory options (like curbing rare earth exports (reuters) carry self-harm. The history of trade negotiations shows that breakthroughs often happen at the brink.

Moreover, some adjustment is already happening organically: firms had begun “friend-shoring” away from China during the U.S.-China trade war and COVID disruptions. The 2025 tariffs accelerate this. In the short run, that means higher costs; in the long run, it means more diversified and possibly domestically rooted supply chains. Export-heavy economies are also likely to stimulate their own domestic demand under pressure, which is a rebalancing global economists have called for for years. For example, if Germany wants to avoid U.S. tariffs, it might finally consider policies to boost German imports (e.g. investment in infrastructure or raising wages, steps that would reduce its trade surplus) (americanaffairsjournal). In that sense, Trump’s aggressiveness could force constructive changes abroad that polite diplomacy could not. Even a U.S.-China decoupling, while costly, addresses security concerns that many now recognize (bipartisan consensus in Washington sees reliance on Chinese supply chains as a risk).

None of this is guaranteed or easy. The contrarian simply argues that continuing on the old path was untenable, and that Trump’s tariffs, as disruptive as they are, at least aim to resolve the built-up distortions. As one analysis from a pro-free-trade think tank ironically conceded, if a country keeps defending big trade surpluses, “there remains no incentive whatsoever” for its partners to make new trade deals (americanaffairsjournal). By that logic, the U.S. had no incentive to keep playing by rules that yielded perpetual deficit. Now Trump has given other countries a strong incentive to negotiate new rules, under the shadow of tariffs.

In the end, what most mainstream analysts missed, perhaps due to ideological bias or simply the inertia of old thinking, is that Trump’s tariff strategy is not about autarky or reverting to 1930s-style isolationism. It’s about forcing a renegotiation of global trade arrangements that have gone unchanged since the Cold War. Just as the Bretton Woods architects sought to create a system to fit the 1945 world, Trump is attempting, in his brash way, to reshape the system for a 2025 world of multipolar economic powers and new rivalries. A former Trump adviser described it as “seismic… a pretty significant shift in the way that we trade with every country on earth” (reuters). The initial tremors are unnerving, but they may give way to a more stable foundation.

Perhaps the fairest conclusion is that Trump’s tariffs are a high-risk gambit – but one born of real strategic insight: that the U.S. had been playing a game rigged against it for decades, and only a dramatic move could reset the board. Most of the commentariat cannot look past Trump’s persona or the short-term market chaos, and so they dismiss the strategy outright. Some, however, see a potential paradigm shift. If Trump’s bold tariffs succeed in compelling major trading partners to strike fairer, more reciprocal deals, or in realigning trade to reduce dangerous dependencies, then this moment will indeed be, as Trump heralds, an “economic revolution” with “historic” results.

What do you think?

Anyways, thanks for reading, that’s all for now.

-Dmitriy